Chapter 6

Agribusiness Hypercommunication Needs

Variations in the scale of production, in rents, and in profits . . . take place from unevenness in the distribution of population, not in the sense of the existence of certain areas where it is on the whole more dense, but in the sense that the markets of different sellers fit into each other in highly irregular fashion. [Chamberlain, The Theory of Monopolistic Competition, 1936, p. 198, italics mine]

Although they were written sixty years ago, Professor Chamberlain's remarks fit what Florida agribusinesses face today as the four legacy communication markets (telephone, enhanced telecommunications, private data networking, and Internet) converge into one hypercommunications network. Variations in profits and the scale of production are apparent in differences in the availability, service quality, and pricing of hypercommunication network access throughout Florida. For example, in downtown Miami, more than fifty competing carriers (with six competing infrastructure technologies) offer many kinds of high-speed access for voice, data, and Internet. However, in other places, choice is restricted to a single ILEC that offers POTS (Plain Old Telephone Service), barely capable of supporting 28.8 kbps modem transmission over analog lines.

Population density alone does not explain such differences in production scale or the enormous variation in profits and pricing. In short, the hypercommunications marketplace in Florida fits Chamberlain's pattern of "markets of different sellers" that "fit together in highly irregular fashion". Chamberlain's original analysis applied to the location problem where retail or wholesale customers travel to a seller's store to shop and buy. Sellers had two economic objectives. The first objective was to select the best store locations given a specific density of customers. The second objective was to discover what product mix would maximize the sales and profits of each location. Customers, in turn, would be "pulled" into visiting the store with the best combination of location and product mix.

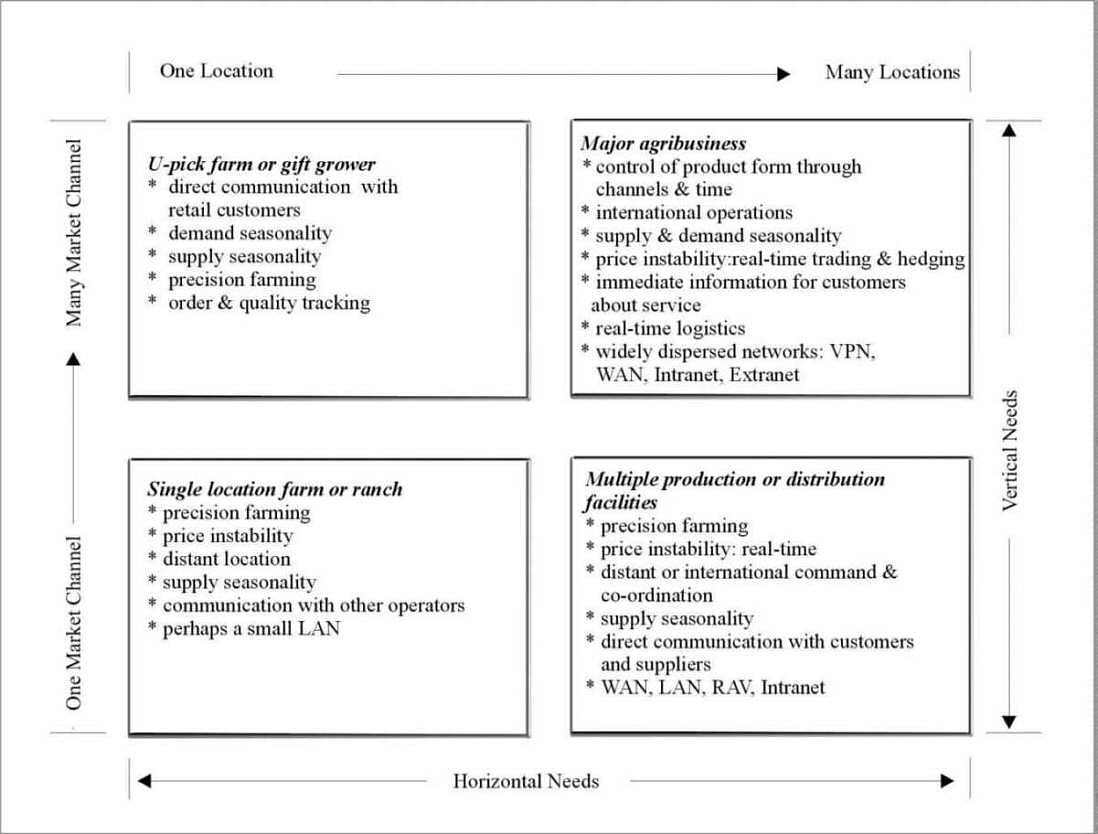

In hypercommunications, since a physical wireline circuit (or wireless path) is required, the store location problem becomes a POP (Point of Presence) location problem with additional complications. Bandwidth (communication capacity), data rate (communication speed), and QOS (communication quality) are directly delivered to customers. Figure 6-1 illustrates this by showing the organization of Chapter 6 and Chapter 7 and their interrelationship.

Two parts of the figure come from material presented in earlier chapters. The QOS reference model (at the top) and the conceptual model (at the bottom) weave a context for Figure 6-1 so that the organization of the chapter into five sections is easier to follow. The QOS reference model (from Figure 4-14 in 4.2.3) separates hypercommunications into access, transport, and CPE (Customer Premises Equipment) at agribusiness locations one and two.

The access level is an electronic pipeline that has been (or has to be) built from a transport carrier's POP to each customer (or cluster of customers) in the form of wires, cables, or wireless transmission equipment. The transport level transmits large amounts of information over long distances at low cost to the POP that serves the second agribusiness location. All forms of hypercommunication (telephone calls, e-mail, faxes, data, enhanced telecommunications, and Internet traffic) travel from the sender over an access level, through a transport network, and over another access level to reach the recipient. This is also true when location #2 is a customer or vendor instead of another office. Note that each agribusiness location uses a separate access level based on the access technology and location to reach the transport network.

The POP connects the physical access level (usually built and operated by a specialized carrier called an access provider) with a physical and virtual transport level or carrier network (often operated by another carrier). Open access from any access provider to any competing transport networks can encourage competition at the access level (leading to more and better communications being sold for successively lower prices) as the section on positive network externalities (3.7.2) suggested. However, as the section on negative network externalities (3.7.3) also suggested, unless the costs of the access level are somehow recovered, open access can lead to congestion and other costs not reflected in market prices. Hence, hypercommunication sellers (such as access providers and transport carriers) cannot simply build stores and recover costs when customers visit, they must build an infrastructure to the customer, recovering their costs through an installed customer base.

Recall from Chapter 2 that the hypercommunication network combines the mass and interpersonal communications models into a mesh network that can carry messages ranging from telephone calls to live video auctions. For convergence to occur, two things must happen. First, high-speed, high-capacity access loops must be available to connect users to POPs that second, are capable of replacing the old separate transport networks of the PSTN (Public Switched Telephone Network), the Internet, and private data networks. In the simpler retail store example, buyers pay a cost in time and money to travel to a store that is optimally situated from the store's point of view. However, hypercommunication access providers and transport carriers incur costs of physically connecting to their customers.

However, a transport carrier need not build the costly access level itself to connect prospective customers with its POP. Cooperation between two hypercommunication firms (an access carrier and a transport carrier) may be required to build a communications path to a prospective customer.

An important feature that carries through the figure from top to bottom is the demarcation line that separates CPE owned by the agribusiness from carrier equipment. The demarcation line represents the end of the agribusiness' local network and the beginning of the access level (also called the local loop or last mile). Again, the hypercommunications marketplace differs from the store location example because (in addition to the access provider and transport carrier), the agribusiness must make an investment of its own before it can buy access or transport.

The bottom line in Figure 6-1, labeled COSTS is the conceptual model (Equation 5-1 from 5.6.1). Agribusinesses pay several separate costs for hypercommunications as described by the variables of the model shown: C&I, TAXES, RACC, VACC, RTR, and VTR. C&I stands for the cost of CPE and installation for the equipment needed by an agribusiness to hypercommunicate. C&I normally includes hardware, software, and services on the agribusiness' side of the demarcation line. Access level costs are divided into RACC (Recurring Access Costs) and VACC (Varying Access Costs). Similarly, transport costs are divided among RTR (Recurring Transport Costs) and VTR (Varying Transport Costs).

Recurring costs are most often charged on a monthly basis and are classified as NTS (Non-Traffic Sensitive) since they do not depend on the amount of hypercommunications traffic generated by the agribusiness. Varying costs are TS (Traffic Sensitive) and may be incurred on minutes, kbps, or other units. TAXES include ad valorem, per unit, indirect, and compound taxes and regulatory fees as specifically described in 5.5 and more generally covered in 5.6.4. TAXES may apply to any of the other costs. However, because they depend on the service location of the agribusiness, they are shown with the C&I cost on the agribusiness side of the demarcation line.

Three of the five levels between the QOS reference model and the conceptual model form the sections of Chapter 6. The first, market boundaries (6.1) are specific to each agribusiness' location. The market boundary for a given location represents the choices an agribusiness has from competing carriers for access to hypercommunication networks. Market boundaries answer the question of where access to high-speed hypercommunication network is available. The section shows how regulatory factors and technology-based infrastructure differences (telephone, cable, and fixed wireless technologies have different ranges from customer to POP) combine to create thousands of different local markets in Florida.

The second level, bundling, is covered in 6.2. Linkages among levels are shown throughout Figure 6-1 to underscore the point that access costs and transport costs may be combined under certain bundles with certain carriers, but priced separately for others. Bundling refers to how access, transport, and other hypercommunication services are often defined as composite goods and priced accordingly. Since hypercommunications is such a complicated subject, bundling can be used to simplify decisions so customers do not get lost in minutiae. However, in practice, bundling also can make comparisons between technologies or among carriers more difficult.

The third level in Figure 6-1 focuses on the unique hypercommunications needs of agribusinesses, contained in 6.3. Specific communication needs are behind the agribusiness manager's question, "How come my agribusiness needs hypercommunications?" The diversity of products handled by Florida agribusiness, an agribusiness' position in marketing channels, span of control, and desire to do business globally are sources for many differences in "Who?" needs hypercommunications the most among agribusinesses. Many of the reasons for agriculture's uniqueness are sources of communication needs as well.

The fourth level of Figure 6-1 concerns hypercommunication suppliers. Hypercommunications supply depends on the number, size, and channel position of firms, the conduct and performance of industry players, and regulation. Questions such as "From whom?" an agribusiness should buy and "When?" to change carriers or upgrade CPE to take advantage of converging networks are answered in an agribusiness' choice of hypercommunication suppliers. Details such as "When?" a particular service will be available, and "Who?" (among hypercommunication suppliers) will offer it to a particular location are not easily answered on a statewide basis. Suppliers are covered in section 7.1 along with general guidelines agribusinesses can use in evaluating hypercommunication suppliers.

Section 7.2 (the fifth level) considers convergence, prices, and economic costs to analyze the question of "How much?" an agribusiness should pay for hypercommunications. Specific pricing details for services and technologies change so rapidly and depend so much on competitive pressures in the local markets that too detailed an analysis would become rapidly outdated and could never cover every geographic area. Thus, 7.2 will give broad ranges of accounting prices and make a special effort to discuss certain less obvious (but perhaps more important) economic costs through the conceptual model and an accompanying decision tree.

Technical details that have been left out of Chapter 6 (to retain an agribusiness focus) may be found in other chapters. Because of the complexity of hypercommunications, readers may have to consult technical details in Chapters 3 or 4 or be at a disadvantage. Understanding pricing also depends on an understanding of the asymmetries of taxes and regulatory charges (as discussed in Chapter 5) which can total thirty percent of the bill (or higher) for some hypercommunication services. A key to abbreviations and acronyms is provided to help with the alphabet soup of acronyms and a glossary to help with the sea of jargon that accompanies making business decisions about hypercommunications.

6.1 Boundaries within Florida's Hypercommunication Marketplace

Boundaries define markets. As an agribusiness shops for hypercommunication services, one of the most important tools for decision making is to understand how markets are physically defined. Boundaries are important because in order to buy with hypercommunications, two things must occur. First, sellers must bring services to buyers via an infrastructure, called the access level in Figure 6-1. Second, buyers must have their own infrastructure (CPE) that is compatible with the seller or carrier's network and capable of handling traffic at every agribusiness location. An agribusiness may do business at fixed locations such as branch offices, or warehouses, as well as in nomadic or mobile locations such as fields, customer locations, salespeople's homes or cars, and trade shows. Locations can be in Florida, national, or international.

Since sellers must bring services to buyers various boundaries are set by technology, government, and competition among carriers. This results in the compartmentalization of Florida's hypercommunications market in practice although in theory convergence should eliminate many boundaries. As Mark Jamison mentions " . . . basing communications policies on boundaries--whether they be geographic, technological, or something else--isn't sustainable. And changing the boundaries is often politically difficult if not impossible" [Jamison, February 1997, p. 1].

The Internet is a good example of how new technologies are altering traditional boundaries as Werbach notes:

Governments act by drawing lines, such as the jurisdictional lines that identify which governmental entity has jurisdiction over some activity, or the service classifications that differentiate which body of law should be applied in a particular case. Governments traditionally determine the treatment of new services by drawing analogies to existing services. . . . There are reasons to believe that a simple process of drawing analogies to traditional services will not be appropriate to the Internet. The Internet is simultaneously local, national, and global, and is almost infinitely plastic in terms of the services it can support. [Werbach, 1997, p. 26]

However, this quotation applies to the Internet at the transport level, not at the access level.

Furthermore, Werbach is speaking of regulatory boundaries rather than technical boundaries. Hypercommunications boundaries are of two main types, technical (6.1.1), and regulatory-political (6.1.2). Technical and regulatory-political boundaries (combined with competition for territory by different carriers) create the irregular market boundaries (6.1.3) faced by Florida agribusinesses.

6.1.1 Technical Boundaries

Technical boundaries are based on the underlying transmission technology, electrical engineering, and laws of physics. Technical boundaries affect the transport, access, and CPE levels in the QOS reference model (top, Figure 6-1). Many technical boundaries were covered in Chapter 4. These include wireline conduit ranges (Table 4-7), network protocol efficiencies (Table 4-27), signal conversion and transformation (Figure 4-2), properties of the electromagnetic spectrum (Figures 4-30 through 4-34), and the range of T-1 line codes (Figure 4-44). While the Internet, fiber optic conduit, and other technologies have led to greater flexibility in boundaries at the transport level, methods of network access must still obey the laws of electrical engineering and transmission that create technical boundaries. In general, technical boundaries depend on the carrier and the carrier's equipment, service type, and the agribusiness' CPE.

Technical boundaries vary by the type of access technology as implemented by a particular carrier. This statement can be supported by showing typical coverage areas for several kinds of technologies: mobile 3G (Third Generation) wireless, fixed upperband wireless, wireline DSL, cableco service areas, fiber optic routes, and Internet tier-one connection locations. Examples of several kinds of these technical boundaries are shown in Figures 6-2 through 6-8.

The first coverage area, shown in Figure 6-2, is for two-way GSM mobile 2G wireless in the Tallahassee area [FCC 00-289, 2000, Appendix H]. Note that the very darkest areas (four distinct sites ringing Tallahassee) are enhanced coverage zones where high two-way data rates are supported for mobile users, while the lighter areas support basic mobile telephone service only. Wireless Internet access and two-way data rates of 384 kbps to 1.5 Mbps can be obtained only in the darker areas shown. Users in outlying areas, shown in moderate gray are able to use only mobile telephony service rather than two-way text and data communication. Even further out, in the lightest gray areas, no service is obtainable at all from the company.

Two-way high-speed paging coverage areas for Arch Communications in South Florida are shown in Figure 6-3 [FCC 00-289, 2000]. With the exception of Lake Okeechobee (dark gray), other dark gray areas are extended service areas where two-way pager users may send and receive text and voice pages from anyone with e-mail or POTS service. However, in lighter gray areas, only basic one-way paging is available. Service is not available at all in white areas.

The next technical boundary shows the range of two-way fixed wireless. In this case, the system is the Airwire MMDS system as implemented in the Orlando-Space Coast area as shown in Figure 6-4 [FCC 00-289, 2000]. Figure 6-4 shows varying degrees of MMDS coverage intensity. The darker the circle, the better MMDS coverage is. For example, users in Palm Bay and Indian Harbor Beach (dark areas) obtain higher data rates and better system reliability than do users near Sanford or northwest of Titusville (lighter areas).

Wireline DSL coverage areas are within telco exchange boundaries as Figure 6-5 shows [FPSC, 2000]. Figure 6-5 can be easily misconstrued. While the figure shows (in white) the BellSouth telephone exchanges where ADSL is supported by CO equipment, there is no guarantee that a particular subscriber located in the white area could actually receive DSL. Successful deployment of DSL depends on numerous technical factors such as loop qualification, loop conditioning, absence of bridged taps and loading coils, and distance from the CO as mentioned in 4.7.3.

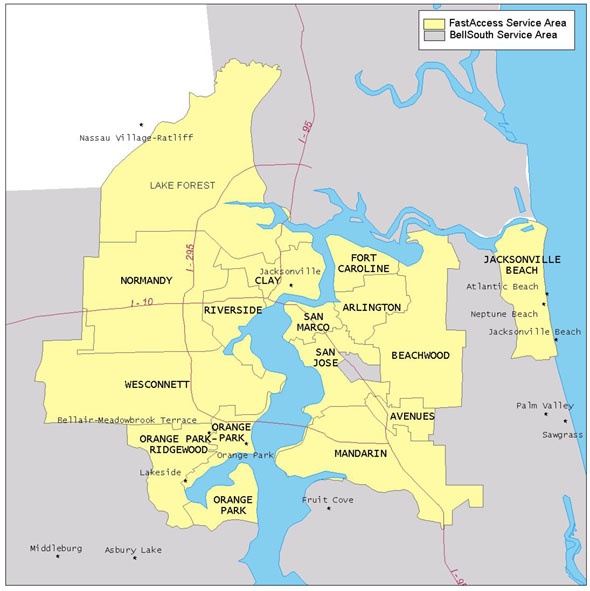

Figure 6-6 shows yet another kind of boundary, the service area of two-way digital cable modem and telephony service by MediaOne (now AT&T Cable) in the Jacksonville area [FPSC, 2000]. Locations shown in gray are those in which two-way cable-based access to "broadband" services are available as of March 2000. Cableco service areas are generally determined by franchise agreements made with local governments both incorporated areas and un-incorporated county administrative regions. Often, ADSL and two-way cable service rollouts attempt to compete for the same geographical market area. However, because cable service areas and telco exchange boundaries overlap (but are not geographic equivalents), market boundaries can become splintered.

Figure 6-7 (from the Desoto County Economic Development Office) shows the high-speed fiber optic infrastructure laid by Sprint in Southwest Florida. The dark line shows the location of the Sprint high-speed fiber optic conduit. Note that Arcadia, Florida happens to be one smaller community through which the fiber optic cable runs. Consequently, economic development efforts for the City of Arcadia area are able to stress the community's closeness to state-of-the art hypercommunications connections as a method of enticing business to the area. Other nearby areas such as Venice, Port Charlotte, and Sebring do not have a direct route through their communities.

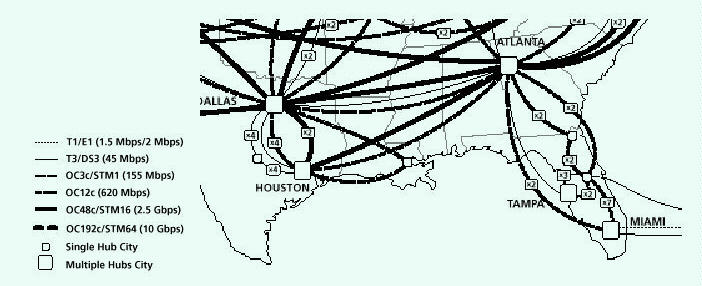

Another kind of boundary concerns the location of Tier-1 or NSP Network Access Points (NAPs) in Florida. Figure 6-8 shows the location of UUNET's (WorldCom) 45 Mbps national backbone hubs [WorldCom, 2000]. In Florida, four places (Miami, Orlando, Tampa, and Jacksonville) are shown as nodes (local hubs) on the UUNET transport level backbone. Tampa and Miami are multiple hub cities. Lines leading from Miami and Orlando offer direct service to the San Juan, Puerto Rico hubs. Atlanta, Dallas, and Houston serve as regional hubs. Indeed, as will be discussed in 7.1.4, many other providers offer major nodes for Internet access in Florida. While most are not located in rural areas, the choice of communications carrier can be important based on how closely linked to the Internet backbone that carrier is.

Figure 6-7 and Figure 6-8 show the location of what are normally considered transport level connections, the location of which traditionally have mattered only to carriers or extremely large agribusinesses. However, fiber optic conduit is used increasingly to bypass access connections (thus eliminating access level costs) or for access to high-speed services such as SONET dedicated connections (Table 4-29). Therefore, as the proximity to NAPs or fiber optic routes grows in importance, their locations will create new technical boundaries.

Although technical boundaries can arise from geographic features, most of the technical boundaries shown in Figures 6-2 through 6-8 are based on the implementation schedules of particular carriers and on general engineering and technological progress. None are static since they can change rapidly with technological changes, new competition, and mergers. It is important to realize that each carrier offers a different coverage area so that those shown in Figures 6-2 through 6-8 are examples of individual carrier boundaries. The set of technical boundaries for all carriers over all access technologies is much larger.

6.1.2 Political and Regulatory Boundaries

The subject of boundaries would not be complete without mentioning political boundaries and boundaries resulting from a mixture of technical and regulatory reasons. Many regulatory boundaries are a direct result of the way telephone service was originally delivered and regulated. For BellSouth (and to a lesser extent other carriers) regulatory boundaries based on telephone technical boundaries from the 1930's are present today in the regulatory boundaries used for POTS (4.6), enhanced telecommunications (4.7), and private data networking (4.8).

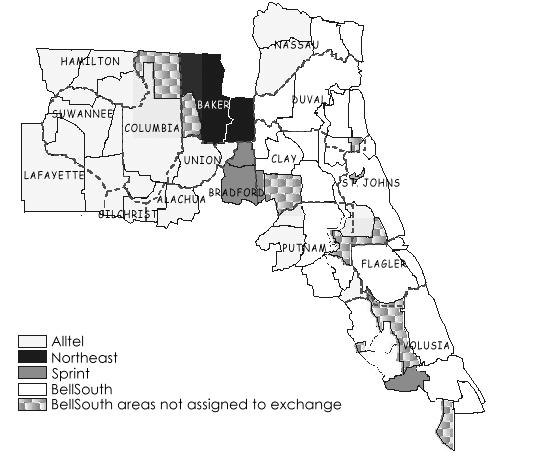

In Chapter 5, Figure 5-5 showed the ILEC coverage areas of Florida to underscore the important role that arbitrary divisions (typically begun in the 1930s and finished in the 1970s) play in the delivery of hypercommunications. In most rural areas, the ILEC has a significant competitive advantage over other carriers based on its traditional status as a monopoly. Figure 6-9 shows the service areas of ILECs by county in the 904 area code [FPSC, 1999].

Inside each ILEC service area in Figure 6-9 are separate telephone rate centers (used to price long-distance calls and define local calling areas) as shown in Figure 6-10 [FPSC, 1999]. It is important to note that rate center boundaries may cross both city and county lines. For example, the Branford, Florida exchange (located northwest of Gainesville) includes parts of Suwannee, Lafayette, and Gilchrist counties. In urbanized areas, rate centers may include multiple cities. For example, the Daytona Beach rate center includes incorporated areas such as Daytona Beach, Holly Hill, Daytona Beach Shores, and South Daytona as well as part of unincorporated Volusia County. Rate centers were defined by the FCC, the FPSC, and telephone companies (originating with AT&T and ending with today's ILECs). While rate centers are becoming obsolete as the transport level changes from a traditional circuit-switched PSTN orientation to a packet-switched computer network orientation, they are still widely used to price long-distance calls and point-to-point data circuits. They are also used to define local telephone service calling areas (as was shown in Figure 4-36).

Each rate center has one (or more) exchanges or wire centers that form the technical boundaries of ILECs. Each exchange has at least one NNX (telephone prefix) that is allocated among various hypercommunications needs like residential telephone service (subsidized by business telephone service), cellular, PCS, dial-up Internet access lines, fax machine lines, and one and two-way pager lines. The Jacksonville rate center (like others in urban areas) is actually a collection of exchanges shown in Figure 6-11 [FPSC, 1999].

In Figure 6-11, the exchanges shown in white have DSL available from BellSouth. By comparing Figure 6-10 to Figure 6-11, it can be seen that not every exchange in the Jacksonville rate center has DSL availability. Exchange and rate center boundaries were established for telephony, but the boundaries for DSL (an enhanced telecommunications service used both for Internet access and telephony) effectively depend on regulatory boundaries designed from telephony regulation.

Figure 6-12 shows two additional kinds of boundaries (LATAs and area codes) that affect ILECs, ALECs, and IXCs [FPSC, 2000].

Florida's LATAs can be seen in Figure 6-12. They include: Pensacola, Panama City, Tallahassee, Jacksonville, Gainesville, Daytona Beach, Orlando, Tampa, Fort Myers, and the Southeast LATA (Vero Beach to Key West). Minor portions of the Savannah, Georgia and Mobile, Alabama LATAs are also within Florida borders. LATAs were designed as part of the 1984 breakup of AT&T, based on telephone exchanges and rate centers. Based on that agreement (and also according to the 1996 TCA), some carriers are allowed to carry voice, enhanced telecommunications, and data networking traffic between LATAs, while others such as Bell South are not. Firms that compete with these ILECs are permitted to carry such traffic. Furthermore, rates on many services are regulated between LATAs in a different way than traffic within LATAs. Within each LATA are a series of EAEAs (Equal Access Exchange Areas) designed to facilitate interconnection among competing carriers. Area codes (NPAs) are shaped by a combination of regulatory policy and the expected teledensity of an area.

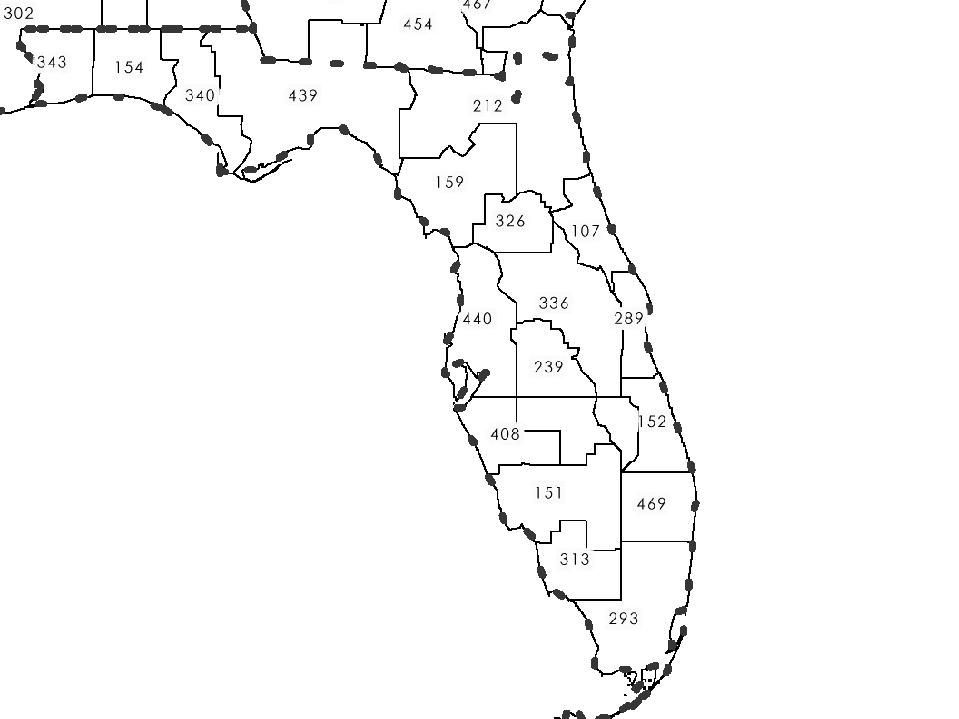

Wireless services follow other kinds of regulatory boundaries from the FCC. Licenses for wireless communications carriers cover mobile services (such as cellular telephony, PCS, and SMR) as well as fixed services (such as MMDS, LMDS, DEMS, and WLL). Each carrier requires a license from the FCC to serve specific territories. Depending on the type of service, FCC rulings may allow one or more carriers the right to serve a specific territory. Often, auctions are used to assign licenses in new spectra to accommodate new wireless services. Figure 6-13 shows the layout of one such territorial boundary in Florida, the eighteen BTAs (Basic Trading Areas) in which licenses for MMDS, Narrowband PCS, Broadband PCS, and LMDS carriers are assigned [FCC, 00-289, 2000].

Other FCC wireless boundaries in Florida include 29 CMAs (Cellular Market Areas) used to grant cellular licenses in, 4 MTAs (Major Trading Areas) used to assign SMR licenses, and 9 BEAs (Basic Economic Areas) used to assign 220 MHz services [FCC, OET, 1999]. However, the right of a wireless carrier to operate within a particular FCC area is no guarantee that the carrier's coverage area will fill that coverage area. To do so, the carrier must construct a series of towers (along with paying the appropriate right-of-way fees to county and local governments) to inaugurate service over the widest area possible.

Finally, it is important to consider purely political boundaries. In Florida, there are 67 counties and 398 incorporated places. Incorporated places are city or town governments with their own police, fire, and other city services, along with several regulatory functions in hypercommunications as given in Table 5-10.

Figure 6-14 shows 28 incorporated areas in Broward County in 1997 [Broward Association of Governments, 1998]. Pure white denotes unincorporated areas. Each area is able to assess local taxes, franchise fees, and other regulatory charges as well as determine which cable television and wireless providers will earn a franchise to provide service. Many incorporated areas have annexed areas of relatively sparsely settled land on the edge of suburbia while certain poorer, longer settled areas contiguous to urban areas of Fort Lauderdale remain unincorporated. Some counties have only one or two incorporated areas, but in fast growing, urbanized areas of other counties, dozens of new jurisdictions have sprouted after 1970. One of the main effects on hypercommunications of local political boundaries is that each local jurisdiction may award a wireline cable television franchise to serve that area. Typically, the proportion of the total franchise area where high-speed access is deployed depends on the cableco's agreement with the local government.

Therefore, political boundaries affect hypercommunication market boundaries in two chief ways. First, a carrier is given the right to provide access to services through the cable TV infrastructure (including telephone, Internet access, private data networking, and enhanced telephony). Second, local taxes are set based on local jurisdictions.

6.1.3 The Meaning of Market Boundaries to Two Agribusinesses

The impact of this patchwork of regulatory and technical boundaries on agribusinesses becomes apparent when the sheer number of different areas is considered. The unique hypercommunications market that a location is in is a function of how the various boundaries described overlap, along with the number of competing firms that operate within them.

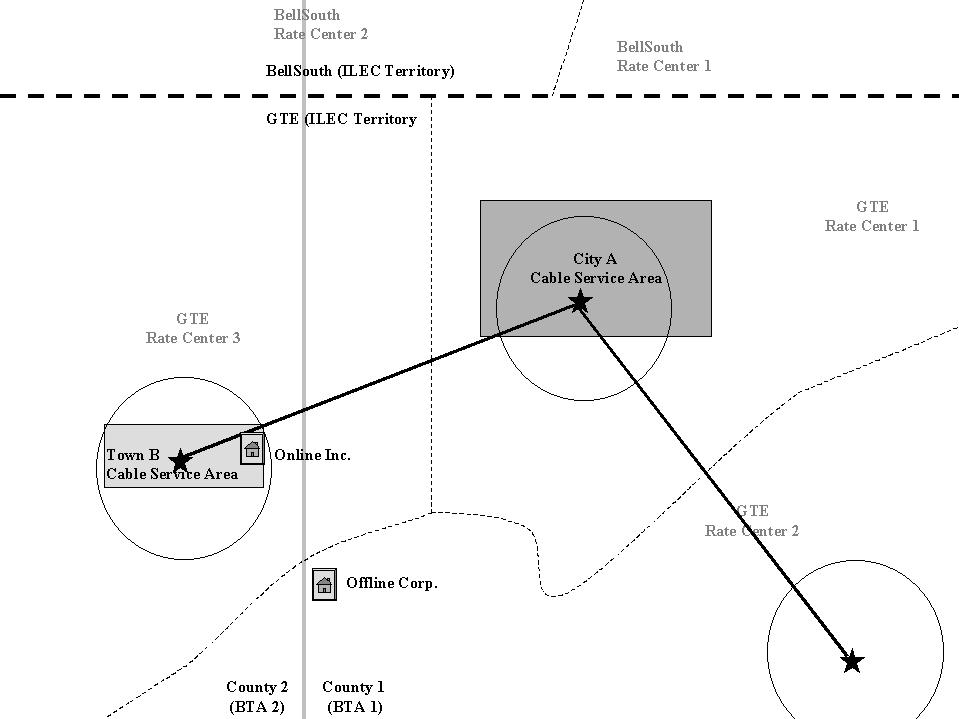

Figure 6-15 explains this point graphically by considering two different agribusinesses, Online Inc. and Offline Corp. Before considering the impact on these businesses specifically, the five kinds of boundaries in the figure need explanation. The first boundary shown is the ILEC territory, shown as a horizontal dotted line near the top of the figure. In the figure, ILEC territories are divided between two ILECs: BellSouth and GTE. Next, within each ILEC's territory are several exchange (rate center) boundaries. Availability of many services and prices for others are based on the exchange boundaries. There are five such boundaries in all shown in Figure 6-15.

Third, the bold star (in three of the rate centers) is the CO for that exchange. A circular area around the star shows the distance limit for deployment of DSL (and other DSL-based products such as HDSL T-1's). Customers must be located inside of the circled area to be eligible to receive DSL. Fourth, there are boundaries of City A and Town B. These boundaries define the coverage area for the cableco. If high-speed access is offered by the cable franchise in either location, assume that it must be within the boxes shown. Fifth, the solid vertical line separates County 2 from County 1. Finally, the solid lines that run from one CO (star) to another show the location of high-speed fiber optic conduit. The location of such high-speed lines is important because high-speed network access can sometimes be bypassed for customers on such main lines but must be kept extremely short if the carrier is to build fiber to the agribusiness location.

Online Inc. will be faced with a different set of prices and choices than Offline Corp. because of the way boundaries overlap. Online Inc. may obtain DSL and HDSL T-1 services from GTE and any ALECs (and ISPs and IXCs) who serve Rate Center 3. Although Online Inc. is on the outer edges of Town B, it may also get service from the cableco. In addition, Online Inc. is close enough to the fiber optic lines that it could use "on net" high-speed fiber bypass services such as SONET or T-3 circuits if it required (and could afford) the capacity. Offline Corp., located just a few miles away, can rely only on the access network provided by GTE to its location, which is too distant from the serving CO to receive most high-speed services. Each firm is in a different BTA, a fact that could create additional competition in both cases if a wireless carrier chose to extend service to these areas. It should be apparent that Offline Corp. has a locational disadvantage where hypercommunications are concerned.

The number of different markets for hypercommunications in Florida is staggering. While not every area is independent of every other, the 461 telephone rate centers, 13 BTAs, 865 active cable TV franchise areas, and 29 CMAs make almost 1,400 different technical, regulatory, and political areas. That is without considering ISP and IXC POPs, ILEC service areas, or the influence of LATAs. Furthermore, the number of possible carriers who may decide to serve a particular location can be large or zero. For example, the 425 ALECs that serve Florida may do so in any telephone exchanges they wish where they have interconnection agreements with ILECs or IXCs [FPSC, August 9, 2000].

While ILECs are required to provide telephone service to every reasonably situated customer within their territories, they have no clear legal requirement (or in some cases permission) to offer enhanced telecommunications or broadband services. In fact, if the former local telephone monopolies concentrate their increasingly stretched resources on building rural infrastructure, they may lose even more ground to new competitors in profitable high teledensity areas. These competitors, who do not have the COLR (Carriers of Last Resort, see 5.5.3) obligations of the ILECs to provide universal service, find a market niche "skimming" off the monopolist's most profitable customers in the cities.

The hypercommunications market in Florida is a classic example of one where "markets of different sellers fit into each other in highly irregular fashion", to quote Chamberlain again [Chamberlain, 1936, p. 198]. However, regardless of market boundary, before a good or service can be priced, the units of price must be defined. Deciding on units is no easy task for hypercommunications as the next section shows.

6.2 Bundling and Other Units of Hypercommunications

Bundling can make understanding the units of in a hypercommunications transaction difficult or easy. Recall that bundling was one of the twelve essential terms introduced in section 1.1. While it is the last to be introduced, it is hardly the least important. Bundling arises now because the economic, technical, and regulatory foundations are out of the way. As convergence occurs, hypercommunications will be sold in bundles of composite goods rather than as separate items such as telephone calls or megabytes of data.

6.2.1 Hypercommunications Bundling

Hypercommunications services can be sold alone (un-bundled) or grouped together in a bundles of services. Bundling may be done for customer convenience, internal billing purposes, due to regulatory edict, to prevent direct price competition or otherwise confuse customers, or in an attempt to protect a supplier's incumbent (or monopolistic) position. The hypercommunications bundle is the quantity that prices are based on.

For example, a local telephone call includes many individual services. These include: the type of access loop wiring, dial-tone, switching, ringing, access level transmission, transport level transmission, busy signal, circuit establishment, connection maintenance, etc. If each component of a call was included separately on the bill for every local call, one call would result in many entries on a subscriber's monthly bill with a separate price for each one. Business telephone bills can already add up to hundreds of pages, but un-bundling every item on every local call would exponentially increase bill sizes. When a technical set of services is too complex for customers to understand in detail, bundling can help buyers understand the general nature of services without confusing them with minutiae. As with restaurant menus, ordering a la carte will still be available but more expensive. The transaction costs of placing, changing, and understanding hypercommunication orders are simply so high to buyer and seller alike that bundling can cut the costs of exchange.

However, bundling can make price comparison among competing carriers a nightmare, especially for less-informed consumers. For example, some customers may not care about (or understand) the difference between an OSP (Online Service Provider such as AOL) and an ISP (Internet Service Provider such as Mindspring). OSPs offer local POP modem dial-up (narrowband) access to a subscriber-based content and e-mail network, with Internet access available (sometimes surrounded by OSP content frames). ISPs offer narrowband and high-speed Internet access, e-mail, data networking, use of ISP servers, and other services through a combination of local POPs for access and national or international backbone peering agreements for transport.

However, it may be very difficult for customers (especially new Internet users) to compare the services between an ISP and an OSP (or to compare providers within each type) because bundling can force a comparison of apples to oranges. Most OSPs and ISPs have several plans which may include unlimited connection or access. That way, subscribers are not charged per e-mail message or by minutes of connection time. But bundles could include (or not include) web site space, 24 hour technical support, choice of billing plans, certain exclusions and limitations, access to CGI and JAVA script files, variations in e-mail features, and guaranteed or as-available connections. The difficulty is compounded when Internet, private data networking, and voice and enhanced telecommunications services may be combined as a single connection.

The FCC and FPSC have prohibited ILECs from reselling only bundled services to competing ALECs in order to foster local telephone competition. During the days of AT&T, bundling was mandatory and often veiled in mystery unless specific legal language was enacted by the states. For example, all telephone sets were leased from AT&T's subsidiary, Western Electric. Access to local and long distance lines, telephone repair and replacement, outside wiring from CO (Central Office) to curb, and inside curb, residence, and business wiring was rolled into one bundle. Operator services such as directory assistance, billing credit (for unconnected, interrupted, or noise-filled calls), emergency (police, medical, fire, call interrupt) were bundled with local service. Per minute charges were levied on only certain services such as long-distance calls.

After the breakup of AT&T, the RBOCs (Regional Bell Operating Companies such as BellSouth) began to unbundle directory assistance, operator services, and inside wire maintenance, while using bundling to sell enhanced services and special calling plans. Bundling, rather than per channel pricing, is how most "non-pay" Cable TV channels are sold as well. Technological trends in carrier hardware and software have made un-bundling easier to implement for hypercommunications customers since new services are increasingly customizable. However, unbundling tends to make billing more complicated. Service bundling is still a popular convenience for many customers, allowing hypercommunications providers to combine sets of services together for special promotions or to induce trial, thus attracting new customers.

However, the ability to bundle services differently from competitors may also be used to make comparison shopping harder and it is arguable that bills are easier to understand. For that reason, bundling strategies of hypercommunications firms are sometimes accused of being anti-competitive. Now, some suppliers such as MCI, AT&T, and Bell Atlantic-GTE are positioned as single vendor solutions for the full range of hypercommunication services. It is possible to purchase wireline or wireless Internet, wireless phone service, local phone service, computer networking, paging, e-mail, voice mail, and long distance telephone services from a single firm that also installs and sells necessary CPE. Such single vendor bundling of sub-industry services into one billed service will be the mechanism that will enable hypercommunications convergence. Some critics allege that this will guarantee less competition in the long run, because the number of firms will be reduced through mergers and acquisitions, leaving only large international firms capable of providing every service. Consequently, it is charged, the remaining firms will obtain a high degree of market power.

6.2.2 Other Hypercommunication Units

The issue of bundling provides an excellent segue into other units used in hypercommunications to construct bundles. Almost all of these have been covered elsewhere, but Table 6-1 summarizes them, shows their location in the text, and summarizes their importance to the agribusiness demander of hypercommunications. Each item may be seen as a different trading unit of hypercommunications or as an ingredient to be used in creating a service bundle.

The most frequently used term of those shown is probably bandwidth. Bandwidth (or capacity) constrains the amount of data that can be sent over a particular link in a hypercommunications link. Closely related are data rate and throughput. The data rate is the single most important factor affecting the price of a communication link. Throughput, while it is related to the speed and capacity of the communications link, also depends on the CPE owned by the agribusiness. The three pertain to all kinds of digital communications from data transmissions to telephone calls and faxes. QOS refers to multiple dimensions of hypercommunications quality and reliability. SLAs are specific guarantees of QOS levels. These concepts are explained in detail in section 4.2.

While the first six units in Table 6-1 are used to create bundles that are sold for an accounting price, the next three items may be more important to determining the economic price. The costs and benefits to an agribusiness of creating, using, and managing information within the organization are not directly priced in markets or measured on the balance sheet.

The last two items, the service primitive and the OSI level, underscore that the networked hypercommunications model of communications (and not the mass or interpersonal model) is at work. The service primitive is merely a way of showing that hypercommunications takes many forms from e-mail and voice mail to interactive telephone or other real-time forms. The OSI model will help show the networking levels involved of a particular service.

However, many decision-makers have insufficient technological training to understand what their Internet options are, much less the full set of hypercommunication units. Often the firm providing hypercommunications services oversells or mismanages its capacity because of the many uncertainties involved in feedforward planning network management. Furthermore, suppliers may deliberately use nebulous units to achieve an information advantage. Therefore, it is especially important for agribusinesses to understand their unique hypercommunication needs.

6.3 The Hypercommunication Needs of Agribusinesses

Agribusinesses have a derived demand for hypercommunication services, based upon profit maximization, cost minimization, or other goals of the firm. An agribusiness manager needs to measure accounting and economic costs, benefits, risks, opportunities, and QOS uncertainties that accompany one hypercommunication choice over another. Unique communication needs for agribusinesses are where the costs, benefits, risks, and opportunities managers are interested in come from. For instance, the needs of a nursery with nine national locations (with both retail and wholesale customers) differ from those of a one-farm peanut operation or a multiple location cattle ranch.

Florida's climate, her geographic setting, her vast areas of arable land, and her people have given it a special place in American agriculture. The state has had many transitions, with agriculture contributing to the earliest ones and responding to the latest ones. This section gives a broad view of some of the unique hypercommunications needs of Florida's diverse agribusinesses. In doing so, a picture of hypercommunication's impact on agricultural input and output markets will also be painted since agribusiness hypercommunication needs depend on factors inside and outside the individual firm. Outside the firm, traditional agricultural sub-sectors and marketing channels as well as innovative new business activities of competitors influence a particular firm's needs. Additionally, the information economy combined with inexpensive global communications creates sources of new customers and new products. Inside the firm, the degrees of vertical and horizontal integration are especially important to hypercommunication needs.

Hypercommunication services are more than ordinary inputs and outputs. Information obtained by an agribusiness and exchanged within it can profoundly affect input and output markets for many goods and services, including those for agricultural products and services. Hence, the pricing and competitiveness of Florida's hypercommunication market has important effects on Florida's agribusiness input and output markets.

There are two chief ways hypercommunications improve agribusiness profits and growth. First, networked hypercommunications can cut the costs of supervision, control, and sales, while simultaneously allowing firms to operate on larger scales or wider scopes. Such results come from changes in the firm's front office (marketing and customer service) and back office (administration and manufacturing) technologies.

Second, information gathered through hypercommunications can change front or back office operations through technology spillovers. Technology spillovers occur when new knowledge is obtained directly and indirectly through hypercommunications, encouraging innovation throughout the firm. Innovation may be from product and systems development (such as a new invention or process that enables increased production while cutting costs or a new idea that frees resources allowing production of new items). Alternatively, the direct innovations may include the creation of information sales or other services. Hypercommunications can also create indirect innovation when new ideas help land, labor, capital, and management become better synchronized and more efficiently used.

This section covers five categories of interrelated agribusiness hypercommunication needs. Before covering those needs, the location and composition of Florida's agribusiness complex is summarized in 6.3.1. The developing agribusiness information economy is the first category of agribusiness hypercommunication needs, discussed in 6.3.2. Hypercommunication needs based on competitive strategies are considered in 6.3.3. Needs based on integration, channel width, and span-of-control are covered in 6.3.4. The fourth category of agribusiness hypercommunication needs (6.3.5) is based on the specific service, crop, or product sold by a particular agribusiness. Finally, needs based on an agribusiness' size or market area are covered in 6.3.6.

6.3.1 Location and Composition of Florida's Agribusiness Complex

Branson and Norvell define an agribusiness as "A firm involved in the production or distribution of agricultural commodities or agriculturally based products, or in the manufacturer and sale of farm inputs." [Branson and Norvell, 1983, p. 509] Agribusiness can be further broken into production agriculture and non-production agriculture to separate the production of raw commodities from the functions provided by the marketing chain.

The specific hypercommunication needs of agribusinesses depend on how broadly agribusiness is defined as well as where agribusiness and its trading partners are located. Communications needs depend on an agribusiness' location compared with its vendors and customers. Therefore, the hypercommunication needs of all agribusinesses (the agribusiness complex) are related to the communication needs of rural areas and production agriculture.

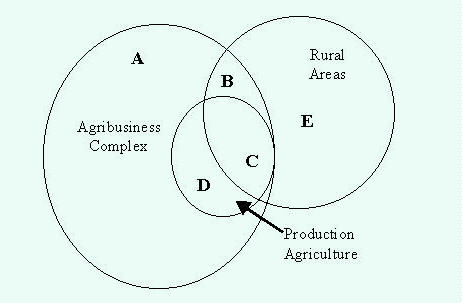

Based on these ideas, Figure 6-16 shows components of the agribusiness complex. In the figure, a distinction is drawn between production agribusinesses (areas C and D) and non-production agribusinesses (areas A and B). A second distinction is made between rural agribusinesses (areas B and C) and non-rural agribusinesses (areas A and D). Area E represents rural communities in general. The agribusiness complex includes areas A, B, C, and D.

All three classifications have elastic definitions that affect the size of the agribusiness hypercommunications market considerably. The definition chosen for each classification alters the size of its circle in Figure 6-16. The combined definitions of production and non-production agribusiness determine the share of Florida's total economy made up by the agribusiness complex. The size of each circle can shrink or expand depending on that category's definition so that there may be differences in the relative importance of rural community infrastructures and non-production agribusinesses not shown by the scale of Figure 6-16.

The rural community circle is the first to consider. As Table 5-2 showed (in 5.2.1), the definition of rural varies, causing the rural communities circle (areas B, C, and E in Figure 6-16) to vary even more than the production agriculture definition. Its size shows both the importance of agribusiness to rural hypercommunication infrastructure development and the importance of the rural markets to agribusiness hypercommunications.

Consider the overlap between agribusiness and rural communities (areas B+C in Figure 6-16). If larger agribusinesses are the earliest adopters of high-tech hypercommunications services and technologies, then infrastructure inadequacies for an entire area might be improved as large agribusinesses demand new services first. Egan argues that business demand drives infrastructure development: "rapid development of an advanced communications infrastructure for rural America will depend on how easy it is for businesses to access the technology" [Egan 1996, p. 284]. The size of the overlaps between non-production agribusiness and rural areas (area B) and production agribusiness and rural areas (area C in Figure 6-16) determines the importance of the rural hypercommunications market on agribusiness communication choices.

If hypercommunications can fade the traditional boundaries between rural and non-rural, then non-geographical spatial elements (such as market structure and technological limits) could become more important than geography. Since the information age makes the world smaller by improving access to previously inaccessible markets, agribusiness interaction with the world becomes more dependent on the geonomics of the access level infrastructure and competition in rural markets. The rural circle is also important to agribusiness communications because of the fixity of assets since an orange grove cannot be moved to take advantage of a more competitive communications market.

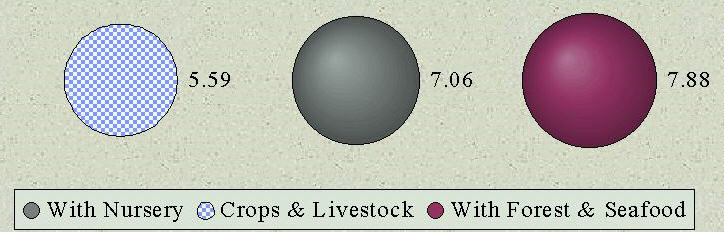

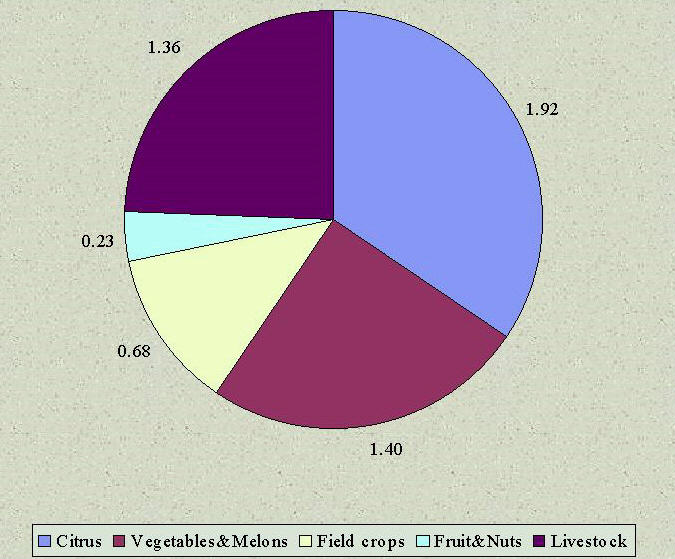

The next circle, production agribusiness, can be three sizes as shown in Figure 6-17. First, production agribusiness may be defined narrowly to include only farms or ranches that produce field crops, vegetables, melons, field crops, and livestock. This conservative definition restricts the definition of production agriculture to traditional farming. However, some non-traditional operations such as aquaculture and horse farms may be included within this definition of production agriculture as well. Cash receipts for producers included by the first definition totaled $5.59 billion in 1999 [Florida Agricultural Statistics Service (FASS), 1999].

Second, production agribusiness may be defined to include all the products mentioned in the first definition along with foliage plants, floriculture, ornamental shrubs and trees, mushrooms, and sod. This expanded definition is important in Florida because the state produces the second most valuable greenhouse and nursery crop of all states in the nation [1997 Census of Agriculture, Ranking of States and Counties, NASS, 1999, Table 35]. The second definition also elevates the role of production agriculture in urban and suburban areas since greenhouses and nurseries are more easily fit into metropolitan areas than row fields and pastureland. Under this definition, Florida had 15,700 full-time farms with an average market value sold per operation of $172,000 in 1997 [NASS, Census of Agriculture, 2000]. Under the second definition, Florida's total cash receipts in 1999 total $7.06 billion [Florida Agricultural Statistics Service (FASS), 1999].

A third, even broader definition, includes the first two definitions, but adds farm woodland receipts and the dockside revenue gained by fishermen (landings). These producer groups increase cash receipts under this third definition to $7.88 billion in 1999 [DOACS Locator, 1997; Bureau of Seafood and Aquaculture Marketing, 1999; DOACS, Florida Agricultural Facts, 1999, p. 71]. The third definition seems appropriate when the total land in production is concerned. The 1997 Census of Agriculture reported that Florida had 10.5 million acres of farmland (some thirty percent of the state's total land area). In 1997, almost 35% of all Florida farmland was cropland, while 20% was woodland and 39% was pastureland [USDA NASS, 1997 Census of Agriculture, 2000].

All firms in production agriculture are agribusinesses. Based on the vast amount of land area in production, it might appear as though most production agriculture operations are in rural Florida (area C of Figure 6-16). Surprisingly, however, over 76% of Florida's production agriculture workers are located in metropolitan areas [USDA ERS, "Florida Fact Sheet", 2000]. In Florida, most urban and suburban production agriculture operations are nursery and greenhouse operations but a scattering of farms that are located in areas where agriculture has been largely replaced by housing are also included.

Production firms typically cannot change their locations at will. This asset fixity is important when considering the market for agribusiness hypercommunications in Florida. Figure 6-18 shows general locations of citrus, vegetable, crops, livestock, and natural agriculture (forestry and fishery) operations [USDA NASS-FASS, Florida Agriculture Facts, 1999, p. I].

However, while the map in Figure 6-18 does not suggest it, many of Florida's most productive production agribusinesses are located in counties with major metropolitan areas or have trading that is geographically concentrated in some other way. This concentration occurs not just within Florida, but within the nation and the world. The location of producers near a metro area may increase their communication options, suggesting perhaps that agribusiness is not as dependent on marginal rural infrastructures as some have suggested. However, while proximity to an urban area may mean that an agribusiness' chances for competitive access to hypercommunications are improved, it does not guarantee a competitive market as the discussion of technical, political, and regulatory boundaries in 6.1 testifies.

The concentration of producer revenue within Florida depends on the commodity as Table 6-2 and Table 6-3 show. Table 6-2 shows the market value of all agricultural crops (on the left side) and the value of nursery and greenhouse sales (on the right side). Each part of the table shows the 1997 ranking of the top Florida counties among all 3,100 counties in the United States. A few Florida counties represent large fractions of total production value as Table 6-2 shows.

Eight Florida counties are ranked among the top 100 counties nationally in the market value of agricultural products sold in 1997. Producers in these eight counties received forty nine percent of total cash receipts for the entire state. Four counties of the eight, (Dade, Palm Beach, Hillsborough, and Orange Counties) are the state's first, third, fourth, and sixth most populous counties (in that order). Florida ranked ninth nationally in the value of cash receipts.

Source: USDA NASS, 1997 Census of Agriculture, Ranking of States and Counties, Table 23 and Table 35.

On the right side of Table 6-2, fourteen Florida counties were in the top 100 counties nationally in the value of nursery and greenhouse crops, Christmas trees, mushrooms, and sod. Five (Dade, Broward, Palm Beach, Hillsborough, and Orange) of the state's six most populous counties appear among the fourteen. Only Highlands County is not part of a Metropolitan Statistical Area (MSA). Together, the fourteen counties represent eighty-one percent of total nursery and greenhouse cash receipts. Florida ranked second nationally, behind California.

In Table 6-3, production is even more concentrated among ranked counties. The table shows the value of vegetables, melons, and sweet corn (on the left side) and the market value of fruits, nuts, and berries (on the right side). Florida is ranked second nationally, behind California, in both categories.

Source: USDA NASS, 1997 Census of Agriculture, Ranking of States and Counties, Table 33 and Table 34.

Vegetable, melon, and sweet corn producers in the thirteen ranked counties were responsible for ninety-one percent of Florida's total cash receipts for those crops. Again, four of the state's six most populous counties are on the list. Two counties (Hendry and Suwannee) are not located in MSAs. The market value of fruits, nuts, and berries (on the right) captures mainly the influence of the citrus crop. Nineteen Florida counties are ranked in the top one hundred nationally in this category. Producers in those ranked counties make up over 96% of fruit, nut, and berry cash receipts. This category includes only two of the six most populous counties, and only Hillsborough makes a large contribution. Seven counties (Hendry, Desoto, Highlands, Hardee, Indian River, Okeechobee, and Glades) are not located in MSAs.

Tables 6-2 and 6-3 suggest four important points about hypercommunications and production agribusinesses. First, while county-level data cannot distinguish between the subtleties of urban and rural areas (as 5.2.1 mentions), county-level data can be used to suggest that many production agribusinesses are located near a metropolitan area. However, although many of the most productive agricultural parts of Florida are within the local calling area of a metropolitan area, that does not guarantee they will have high-speed hypercommunications access. Nonetheless, producers in MSAs (an especially those in the most populous counties) are in a better position than those in other parts of the state to receive high-speed wireless access. Depending on local boundaries, these MSA producers are also more likely to have several choices for wireline access now or in the near future.

Second, the ranking data suggest that production agriculture (in general) and the citrus industry (in particular) are less concentrated in MSAs. Thus, if high-speed access and competition in hypercommunications are related to county density, some sectors of production agriculture will fare worse than other sectors in the next few years. A third point concerns the difference between revenues and the number of operations. Tables 6-2 and 6-3 use rankings based on revenues, not farm numbers. Rankings based on countywide revenues do not tell anything about the total number of operations.

Fourth, the tables suggest possible differences in access among producers of a particular crop based on location. A nursery in Broward County probably has (and will continue to have) better access and more hypercommunications choices than will a Gadsden County or Highlands County nursery. To the extent that hypercommunications give producers a business advantage, that advantage may come only to producers who are located in advantageous locations to begin with. It is important to note that advantageous locations may be based on factors such as transportation routes and distance to market that are positively correlated with hypercommunications advantage.

The rural circle and the production agriculture circle shown in Figure 6-18 have now been covered. The analysis above suggests that the rural circle may represent a somewhat smaller part of production agribusiness than would be expected in other states. However, many agribusinesses cannot be classified as production agriculture. The third circle, non-production agribusinesses, makes up four basic areas: farm input suppliers, processors and marketing firms, wholesale, and retail operations.

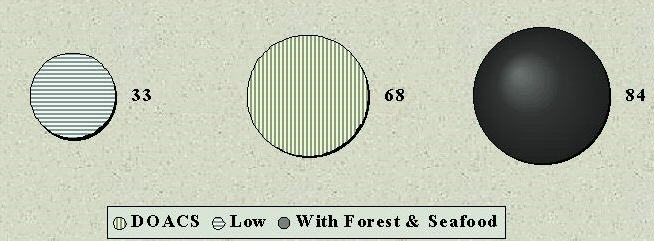

Again, there is a question of how broad the definition should be. According to Florida's DOACS, the agribusiness complex contributes $20 billion in direct farm-related economic impact on the state and $55 billion in direct and indirect value added from the farm gate to the supermarket [DOACS, Florida Agricultural Facts, 1999, p. 1]. Forest and forest products contribute an additional $8 billion to the state's economy, while the seafood industry adds $1.4 billion to the economy [Jacobsen and Vericker, 1998; Bureau of Seafood and Aquaculture Marketing, 1998]. Thus (as shown in Figure 6-19), depending on the definition of the production that underlies their efforts, non-production agribusinesses add between $33 billion and $84.4 billion to Florida's gross state product. With Florida's gross state product estimated at $400 billion, the agribusiness complex contributes from eight to twenty-one percent of that amount.

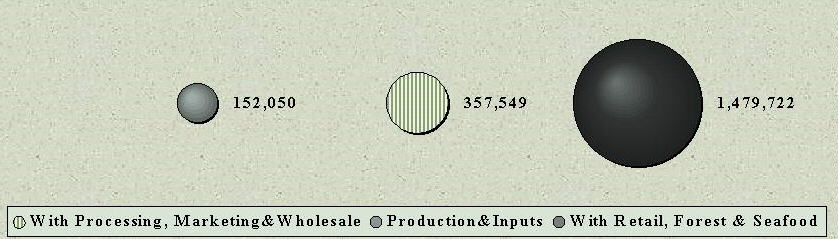

Most non-production agribusiness employment is in non-rural areas. According to the ERS and other agencies, 14.2 percent of total metro area employment was in farm and farm-related jobs while 22.1 percent of total non-metro employment was in farm and farm related jobs in Florida during 1996. When extrapolated onto 1998 total employment, this translates into over 1,100,000 employees of metro agribusinesses and almost 99,000 employees of non-metro agribusinesses in 1998 [USDA ERS, Florida Fact Sheet, 2000]. When employment in forest products and the seafood industry are added in, the total climbs to the 1,479,722 employees as shown in Figure 6-20 [Jacobsen and Vericker, 1998; DOACS, Florida Agricultural Facts, 1999, p. 75; DOACS, "State of Florida Facts", 2000].

The broadest definition of an agribusiness in Figures 6-19 and 6-20 would include the communication needs of retail outlets as wide ranging as grocery stores, restaurants, and furniture showrooms. However, the narrowest definition might exclude important parts of the agribusiness complex that are responsible for adding the most value to food and fiber producers output. Clearly, the more people employed by the agribusiness complex, the greater the need for hypercommunications and the greater the size of the agribusiness hypercommunications market.

However, there is no definitive answer to the size of the agribusiness complex. The relative sizes of production compared to non-production and the overall size of the agribusiness complex give different pictures of the extent of the hypercommunications market. Many hypercommunication needs do not depend on the size of the agribusiness hypercommunications market but on the unique characteristics of agriculture and specific characteristics of individual firms. Before considering some of the more specific needs based on competitiveness, vertical-horizontal integration, agribusiness type, or size of agribusiness, the next sub-section considers the needs of the agribusiness sector as a whole.

6.3.2 Unique Characteristics of Agriculture and Agribusiness Hypercommunication Needs

It is often said that agriculture is a unique industry. While that is true, in many ways, the discussion in Chapter 2 of the three foundations of the information economy (communication, technology, and information) applies to agribusiness just as it does to other industries. Some have argued that extractive industries such as agriculture and mining are somehow not part of the new "weightless" economy [Rawlins, 1992]. In spite of those arguments, many agree that over the past decade agriculture has evolved into "an information-intensive food production system" [Saxowsky and Duncan, 1998, p. 5].

Taylor and Fairchild explain how IT will transform agribusinesses:

Perhaps the most profound impact on trade and competition will be created by changes in information technology. Supply chains evolve to minimize the cost of information flow and its management, thus transactions costs along the supply chain have been altered by access to real-time information at very low cost. Examples include the decline of traditional wholesale distribution channels and the increase in vertical and horizontal strategic alliances in the fresh fruit and vegetable sub-sector. [Taylor and Fairchild, 2000, p. 2]

Hypercommunications provide the raw data from which agribusinesses glean information they need to learn about and respond to customer needs, buy and sell inputs and outputs, perform business intelligence, and manage multiple locations. The objective of the information intensive agribusiness is to gain an economic advantage in an increasingly competitive international market by minimizing the cost of bandwidth (capacity) while maximizing information literacy and improving the efficiency of information handling. The intended result is asymmetric information or an informational advantage that can be used to raise profits, increase sales, find new products, enter new markets, and lower costs.

Given the importance of the infor mation economy to agribusiness and the importance of hypercommunications access and transport to information acquisition, many unique characteristics of agriculture create specific hypercommunication needs. Table 6-4 lists eighteen unique characteristics of agriculture, describes each one and related agribusiness hypercommunication needs.

Not every item in Table 6-4 is unique to agriculture. Other industries have instability, asset fixity, and environmental concerns, and share many of the economic characteristics mentioned with agriculture. The true uniqueness of agriculture (and the source of many unique agribusiness communication needs comes) from the fact that the combination of characteristics in Table 6-4 and interaction among them are specific to agriculture alone.

The first unique characteristic to agriculture is the uncertainty biology brings to production. Tweeten describes this as the "unpredictable and uncontrollable influence of weather, insects and other pests, diseases" and the resulting impact they place on producers and non-production agribusinesses alike [Tweeten, 1989, p. 20]. Having better information can prevent or reduce risks, while improve timing and efficiency. Hypercommunication is especially important because it provides the pipeline information flows over to reach farms and ranches that require an increasing amount for precision agriculture or other high-tech information-based production needs.

Source: some characteristics are based on Tweeten, 1989, pp. 1-31.

Biological uncertainty brings specialized hypercommunication needs to non-production agribusiness also. Having better information about weather and other uncertainties faced by producers that can create potential supply shocks helps marketing firms plan evasive action. Such evasive actions include increasing stocks, increasing storage capacity, searching for alternative suppliers, and changing recipes or formulas. Information about competitors' actions and technology transfers also helps non-production agribusinesses weather supply shocks due to biological uncertainty, even helping with invention of new products and processes that improve an entire operation or product line.

A second unique characteristic is the inelastic short-run price elasticity of demand of food at the industry level and for many individual agricultural products. The main reason for the short-run demand price inelasticity is that food products are essential to human and animal life [Tweeten, 1989]. In emergency conditions such as hurricanes or other disasters, restoring communications to agribusiness to ensure a steady food supply can prevent famine and public unrest. For this reason Florida disaster preparedness instructions for communications restoration rank non-production agribusinesses (retailers, wholesalers, and middlemen) behind only law enforcement and health care as an essential service. Larger agribusinesses and retail operations need to have robust, redundant communication systems because of the importance of food to society.

Food security is important to national security. Thus, international agribusinesses, food aid, and food policy require effective and efficient transportation and communications infrastructures. IT and hypercommunications can allow cheaper and more effective timely international communications than ever before. However, foreign infrastructure and the protection of national PTT (Post, Telephone, and Telegraph) monopolies can hamper the ability of agribusiness and NGOs to communicate cheaply.

Another unique characteristic of agriculture is price inelastic short-run supply. Once crops or trees are planted or breeding stock is purchased, suppliers cannot adjust quickly to changes in price. For example, once a field crop has been planted and starts to grow biological processes take over, and farmers cannot change short-run supply response to price as well as producers in many other industries can. The impact hypercommunications can play in mitigating negative effects of this characteristic is major. For example, localized real-time information about planting intentions could allow producers to form more informed expectations, possibly helping to reduce the chronic oversupply that plagues U.S. agriculture.

A fourth unique characteristic of most agricultural products is that income elasticities of demand are low [Tweeten, 1989]. As incomes rise, much of the increase is spent on goods and services not related to the agribusiness sector. Therefore, growth in demand for food products must come from overseas markets or from population growth rather from better economic conditions.

However, new methods of marketing and positioning agricultural goods and services can counteract this. Direct marketing techniques, agri-tourism, eco-tourism, recreational tourism, and niche product positioning can be used to keep some production agribusinesses in farming by diversifying operations and improving bottom lines [USDA AMS, 2000]. These techniques require a high dependence on hypercommunications especially because such agribusinesses must have the ability and capacity to handle more communication directly with consumers than they are accustomed to. Non-production agribusinesses may have to vertically integrate (and even establish retail arms) as IT alters the supply chain. Better communications are at the heart of both strategies. In both cases, better customer service, customized products, and real-time information are needed to appeal to and serve high-income customer demand. Such a strategy can help counteract both low income elasticities of demand and the next characteristic, price taking.

A fifth characteristic of agriculture is that individual producers face an extremely price elastic demand. Producers have little market power so they are dependent on prices that are set in spot, futures, forward, and options markets. By altering the marketing strategies of the agribusiness (by offering custom services and personalized products aimed at high-income groups as described above), a producer may become a monopolistic competitor with somewhat more control over price. Additionally, even for commodity producers and marketing firms that depend on open market pricing, better information can help the timing of buying, selling, storage, and other decisions to lessen the effect of price instability. The Internet has created a revolutionary increase in the availability of real-time information about markets and prices along with new markets. Transaction costs have plummeted, while the amount of available information has grown faster than the costs of access and transport have fallen. However, it can be hard to evaluate the quality of large quantities of information.

On a related note, agriculture's next unique characteristic is its "high dependency on precarious foreign markets" [Tweeten, 1989, p. 21]. The DOACS reports that for U.S. fiscal 1997-98, almost $1.1 billion dollars worth (16.3% of cash receipts) of production-level crops were exported from Florida. In addition to new foreign markets for citrus juices, increased competition with Mexico in tomatoes, squash, snap beans, cucumbers, bell peppers, and other vegetables shows Florida producers and processors that the domestic market is really a world market. However, Florida's strategic position near Latin American growing markets and the promise of improved trade with the Caribbean and Africa should see its rank climb from the 17th leading U.S. agriculture export state. Not to be ignored is the importance of foreign markets as a source of production inputs and ingredients for non-production agribusinesses.

Several hypercommunication needs stem from the importance of global markets on agribusiness. Most importantly, lower costs of communications with overseas (especially via the Internet) allow even small agribusinesses to seek new buyers or vendors anywhere in the world. While the importance of global markets varies by crop, hypercommunications also allow agribusinesses to be well informed about international markets, import and export regulations, and gives them closer contact with foreign agents or salespeople. While inexpensive hypercommunications increases international communications, this is one area where middlemen (such as export brokers and importers) could see their roles grow due to the red tape involved in international trade.

The seventh unique characteristic discussed in Table 6-4 is fixity of assets. Much of the capital equipment used in agriculture may be specific to agriculture only or even to a specific crop or animal. While many agribusinesses are leaving agriculture or moving operations as urbanization swallows up vast tracts of arable land in Florida, some land is so remote or otherwise unsuitable for development that it too must remain in farming or become idle.

While hypercommunications does not alter the physical reality of asset fixity or reverse urbanization, two communication needs relate to this characteristic. First, assets that have to be sold may be more liquid since the Internet can increase the seller's audience size substantially, broadening the extent of the market. Second, to the extent that an improved hypercommunications infrastructure can help agribusinesses increase returns on land, it is possible that more land will stay in agriculture instead of being converted to urban uses.

Another unique characteristic of agriculture is the importance of lobbying, government relations, and public relations. Many federal and state policies are specially targeted to agriculture so that both production and non-production agribusinesses have special communication needs based on their membership in a common political network with similar interests. The importance of the family farm to U.S. farm policy is one example of a message that goes across commodity lines. In many other cases, segments of agriculture work at cross-purposes. Agriculture's story is cheaper to get across over the Internet due to low per unit costs of web pages and legislative alert e-mails. However, agriculture's story is also harder to get across through the clutter of increased message traffic.

Producer associations, trade groups, and farm organizations are using the Internet (along with Internet site design and promotion suggestions such as those given in 4.9.3 through 4.9.5) to defend, explain, and educate the public about Florida agriculture. Organizing letter campaigns or other efforts among members of a human network connected by a common communications network with a choice of message types (like the Internet) is cheap, effective, and simple.

The ninth unique characteristic is agriculture's effect on the natural environment. While other industries affect the environment, production agribusiness is unique because it occupies more land area than any other industry. Farming practices such as agrochemical use, monocropping, soil conservation, wetlands reclamation, land use, water use, and others influence the overall natural environment. In Florida, many of these practices are under attack, such as the controversy regarding the alleged contamination of the Everglades by sugar operations and dairies. Just as with the public relations-government characteristic just mentioned, hypercommunications (especially the Internet) allows agriculture to get its message out quickly and cheaply. It is easier than ever for agribusinesses to explain their positions and educate the public through group or individual action. The Internet creates new venues of debate and opens (through e-mail and other technologies) new methods of communication. Also important is environmental education of farmers themselves, made cheaper for extension and other interest groups.

Another unique characteristic of agriculture is the importance of food safety and healthfulness. In reality, this characteristic covers several areas. First, agribusinesses have a legal and ethical responsibility to provide safe food products throughout the distribution chain. Second, since food is how human nutrition is satisfied, information about the nutritional content, best ways to prepare, and information about disease fighting properties of food are important to the public and news media alike. A third area important to non-production agribusinesses especially is the burgeoning nutraceutical market.

These areas give birth to several hypercommunications needs. First, the ability for an agribusiness to communicate the details of a food recall swiftly and accurately to retailers or other distributors is important. Since communication is a two-way process, handlers or other manufacturers must be able to answer questions about a recall or food safety scare from other agribusinesses, the news media, and the public in as uniform and accurate a manner possible. Interactive web sites, e-mail response teams, emergency communications policies, real-time inventory location networks, and telephone hotlines are some examples of specific tactics that might be necessary. Now, such techniques do not require a large staff or a big budget to implement.